Business

A Layman's Guide To Credit Card Fees And How To Reduce Them

Dodd Caldwell

July 21, 2020

Credit cards are convenient, popular, and faster than checks or cash. It’s no wonder that a large (and growing) percentage of consumers are using them for all kinds of transactions.

But as a business owner, you deserve to know about the effects credit card fees will have on your business and how to alleviate the impact. And, as our society moves more and more to paper-free transactions, it will become more and moreshu important for merchants to accept credit cards.

The best way to have a stable business in this credit card age is to know what the fees involved are and how you can find creative ways to save on them.

A Brief Introduction to Credit Card Fees

Credit card fees can be an extremely complicated and overwhelming task for a new entrepreneur. This section will only cover the basics, as that’s all you need to know for right now.

However, a word of comparison: One of the reasons MoonClerk exists is to simplify the process of accepting credit card, including not having to worry about what your actual processing fees may be (more on that later.) MoonClerk offers built-in software that is ideal for both one-time and recurring payments. If you feel another platform is right for you, this introduction will be your crash course in what you need to know.

However, just by finding a bank with a lower transaction fee doesn’t mean you’ll have the software to accept recurring payments. But with MoonClerk, you get all that and more, right out of the box!

OK, so if you’re not using MoonClerk, there are four major players in every credit card transaction beyond the consumer and the merchant (you):

- The Issuing Bank is the organization that provides the physical card. Think your bank here. Examples include Citi or Bank of America.

- The Credit Card Association or Credit Card Brand is the credit card company. They create the cards. Examples would be Visa and MasterCard. They, along with issuing banks, determine most of the fees you will pay for using their cards.

- Acquiring Banks hold the accounts for businesses who accept credit cards. Their job is to reimburse customers if the business goes under, so they act as a layer of consumer protection. Chase and Wells Fargo are examples of these banks.

- Processors are a diverse and complicated category of individuals and organizations that actually push the transactions through and handle various aspects of sale and service.

Credit card fees fall into three major categories:

- Transaction fees are charged per transaction and are paid to the issuing bank and the credit card association. In other words, to your bank and the credit card company. These fees break down into two smaller categories:

- Interchange fees: paid per transaction and are a percentage of the sale plus a small fixed amount, like $0.10.

- Assessment fees, which are paid to the credit card company each time a business accepts a debit or credit card from their brand. They are a small percentage of the transaction (based on monthly volume), and an additional small fee.Both kinds of transaction fees are nonnegotiable.These will account for the largest cost you will incur in accepting credit cards.

- Flat fees are various additional fees charged by your processor for using the card and any other services or equipment. They include things like terminal rental, eCommerce fees, early termination penalties, and so on. These vary greatly depending on provider and are an important part of picking which company to work with.

- Incidental fees are like flat ones. They vary and depend on your processor. They are less frequent and depend on exactly how you use credit cards. Address Verification Service (AVS), retrieval request fees, chargebacks, and voice authorization fees all fall into this category.

Are you confused yet? If you want a far more in-depth discussion of all the minute ins and outs of credit card fees and how they work, Simple Dollar and Merchant Maverick have great crash courses!

But, here’s where all this information impacts you: Remember how I said you can’t change the transaction fee cost? Well, you can change the costs of flat and incidental fees.

Most credit card experts call the former “wholesale” costs, which are nonnegotiable, and the latter are “markup” costs, which most certainly are negotiable.

To start saving money on transaction fees, your goal should be to find a processor who gives you the most quality service for your money while charging you the smallest possible markup fees.

And the cool thing is, to quickly and safely cut out all of this confusion, you can just use MoonClerk. They do all the work for you while offering you easy set up, built-in software, and a secure processor undergirding every transaction.

Navigating Markup Fees

Processors charge markup rates differently. There are three major pricing models, the first or last of which can be the most merchant-friendly:

- Flat Pricing is commonly used by many processors. It’s called “flat” pricing because the processor takes flat rate from each transaction and deposits the rest in your account.You may hear that flat pricing costs more than pass-through. This is not necessarily true; other merchant accounts charge additional fees atop their standard transaction costs, which end up being more than the one simple cost from flat fee processors. Thus, the lower listed price may not actually be lower, if your processor adds many fees atop that.That isn’t the case with Stripe, the processor which underlies MoonClerk’s software. Further, larger volume transactions can get an adjusted transaction fee from Stripe easily. With MoonClerk, you’ll know what you’re paying ahead of time and won’t be surprised by hidden surcharges or fluctuating percentages. (Stripe charges the transaction fees, while MoonClerk charges a monthly rate based on transaction volume.)

- Bundled Pricing should be avoided if at all possible. In this scenario, the processor is paid directly—they then pay the transaction fees, while keeping whatever is left over for themselves.They can charge you whatever they want and you have no way of knowing exactly how much you’re paying in markups or if those charges are fair and necessary.

- Pass-Through Pricing emphasizes transparency. The transaction fees are “passed through” directly to you, the merchant, while any markup fees are charged separately.This way, you know exactly what your processor is charging and they can’t add hidden fees. Additionally, it also ends up being cheaper for you to have all of the markups charged separately.

While pass-through costs merchants less money, in some instances flat pricing can be the better option given that it is streamlined, user-friendly, and extremely clear.

Deciding which is best for you depends on your business goals, your transaction frequency, your monthly income, and other factors.

9 Tips and Tricks to Save on Fees

Now that you know something about what the fees are and how they’re assessed, let’s look at ways to minimize fees. Some of these will only apply to merchants with a physical store and terminal, while others will apply to everyone who accepts plastic.

1. Set a Firm Minimum Limit

This can be extremely useful. Simply post a sign at the cash register that says you will not accept credit cards if the transaction is below a certain price (say, ten dollars).

There is a touch of psychology here, and it’s beautiful: Most people will prefer to either pay cash or take the advantage of buying more things with their card, instead of having to limit themselves to the small amount.

This works out for you either way: If they use cash, you avoid all processing fees. If they buy a ton of stuff with their card, you may be able to offset some of the fees that you’ll incur.

2. Do Your Homework

Most problems can be avoided ahead of time by researching processors very carefully. Remember that you want to avoid bundled pricing wherever possible and to focus on either flat pricing or push-through (whichever is most conducive to your business).

This is where you have leverage over how much you’re going to be charged for the things you actually can control, so spend as much time on this step as you need.

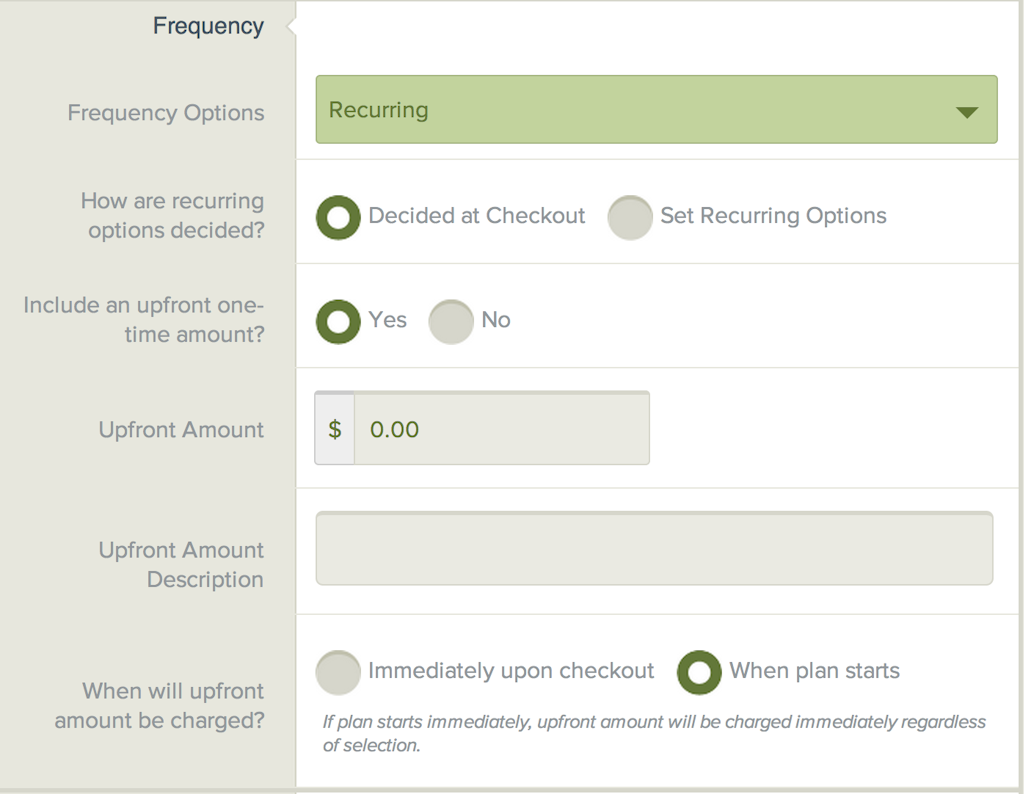

MoonClerk is great for both one-time and recurring transactions. Here’s an example of a business whose recurring transactions grew to thousands of dollars each week.

3. BYOT (Buy Your Own Terminal)

Many processors allow merchants to rent terminals for a monthly fee. This sounds convenient (and it may be for some people), but it ends up being unnecessarily expensive. It’s far easier to simply buy your own—and you can get good ones from any office supply company.

4. Swipe, Don’t Type

This is a mistake that can be made easily if you accept a lot of over-the-phone transactions. Because the physical card isn’t being swiped, it’s easier for fraud to take place and you will be charged extra by your credit card company to set off potential fraud costs. It’s far easier to physically swipe the card and to inform your employees of that requirement.

If you do want to accept non-physical payments, or must otherwise type in credit card information, you can simply make sure you include the CCV (security) code on the back of the card. This functions the same way as if the card was swiped.

5. Use a Giant Bank

This isn’t possible for everyone, but if you can, choose to have your payments processed directly by the issuing bank.

Using a smaller, local bank will actually increase markup costs because they’ll just outsourcing their processing services to one of the larger players like Chase, Bank of America, and Wells Fargo.

Also, the smaller bank will have various overhead costs—like salary, insurance, maintenance, building costs like mortgages or electric bills, and other expenses—that will get passed on to you in the form of higher processing fees. Choosing to have a larger, national entity process your transactions will save you lots of money in the long run.

6. Do It Right From the Start

“Measure twice, cut once” is a cliché for a very good reason. You must make sure that your account with the processor is in order ahead of time and that your terminal is set up properly.

If they aren’t, you’ll just have more charges and fees that you have no good reason to pay.

For those of you that have physical terminals, it’s very important to process transactions quickly, because batch fees will only increase based on transaction volume.

Even waiting a few days can make costs skyrocket unnecessarily. Get in the habit of processing within 24 hours.

The discipline and care involved in taking the extra time to submit the proper information and have everything in working order will pay off nicely.

7. Check With an Expert

It’s natural to feel overwhelmed by all of the moving pieces involved in credit card processing. It’s a good idea to talk with a processing consultation company, as they can help you navigate the jungle and guide you to the processor and rate combination that works best for you.

Besides helping with myth refutation, they can give you the confidence of having an informed expert show you the ropes. One example of this kind of company is Ideal Cost, which originally began as a local firm in Florida but expanded nationwide several years ago.

8. Don’t Be Afraid to Ask

There really isn’t such a thing as a stupid question. As you shop around for processors, don’t be afraid to ask questions about how they charge markups, for what, why, and if they are willing to work with you to lower costs.

A good company will be more concerned with serving you, the customer, than being obsessed with their own profits.

If you get answers that will hurt your business or cost you unnecessarily—or worse, are lied to or evaded—run.

MoonClerk partners with Stripe to do all its processing. Stripe is one of the most popular and reputable processors on the web and charges clear, simple rates for all transactions. Find out more here.

9. Be Sure to Comply

The better credit card processors require merchants to meet a series of industry standards to maintain integrity and reduce security risks.

Payment Card Industry (PCI) Compliance status means you’ve been evaluated and have been determined to be compliant with all of the various requirements and expectations set by the card issuing companies.

Here’s why this is a way to save money: There is an annual fee involved to go through the program (it can range from $90 to $165 per year), but that’s it. With MoonClerk and Stripe, however, PCI compliance is included.

Noncompliance will rack up more charges than you want to even think about, and can cripple or shut down businesses as a penalty.

Get the reputation of being a merchant who has integrity and complies with industry standards. It’ll save you money and headaches—and pay back a sense of honor and confidence.

Conclusion

Credit cards are a permanent and growing way of life for millions of Americans.

Business owners large and small owe it to themselves to navigate the system in a way that will maintain transparency, allow them to grow, and create real profit.

This process can feel scary or bewildering at first, with all the different rules, options, and combinations. But with platforms like MoonClerk and Stripe, all of the guesswork and navigation is already done for you, and an easy set-up and smooth, secure reliability for both one-time and recurring transactions is bundled together from day one! Instead of figuring all this out for yourself, let the experts at MoonClerk and Stripe experts do it for you, and focus on what’s most important: building and securing your business and its future!